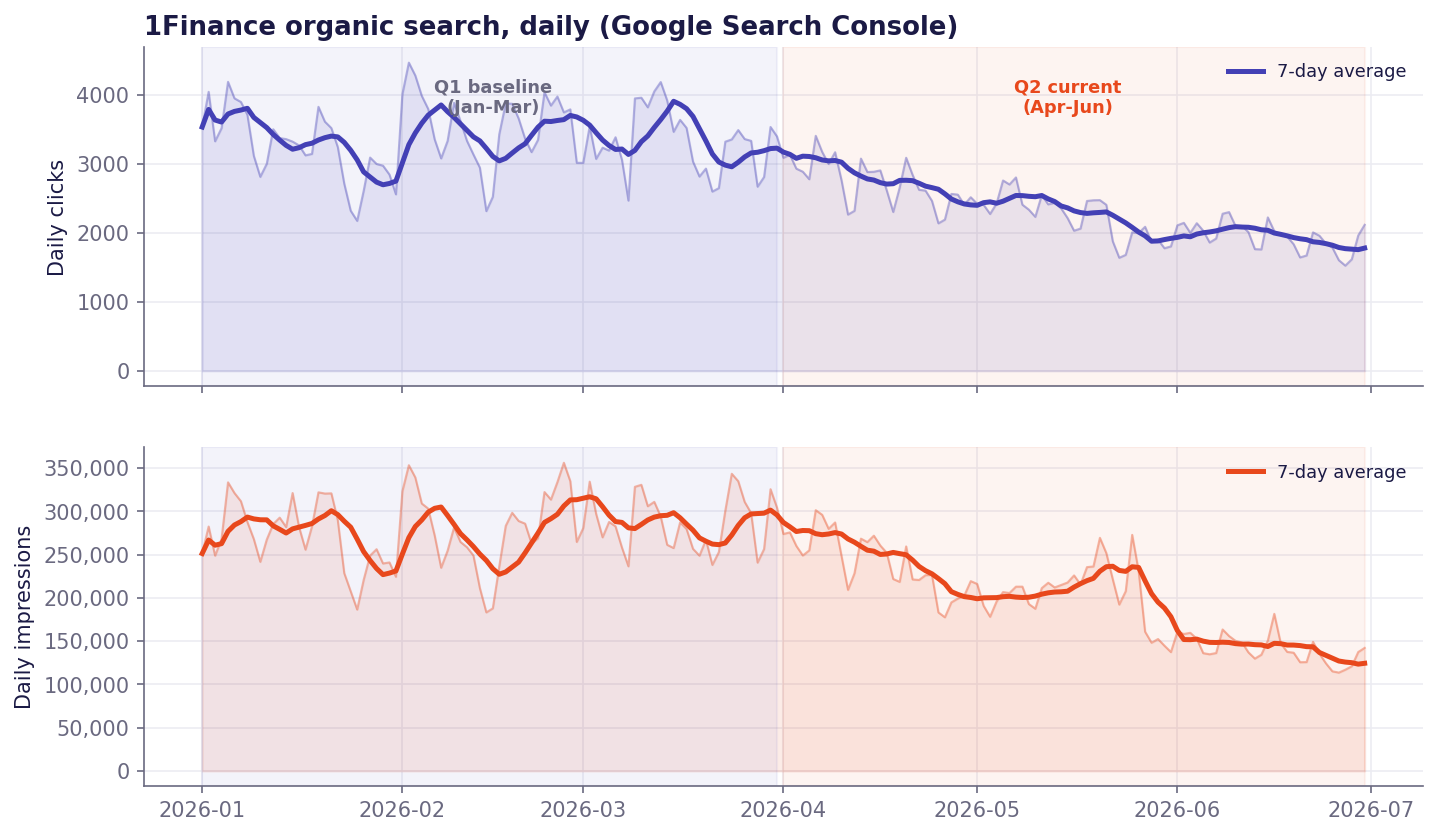

Why

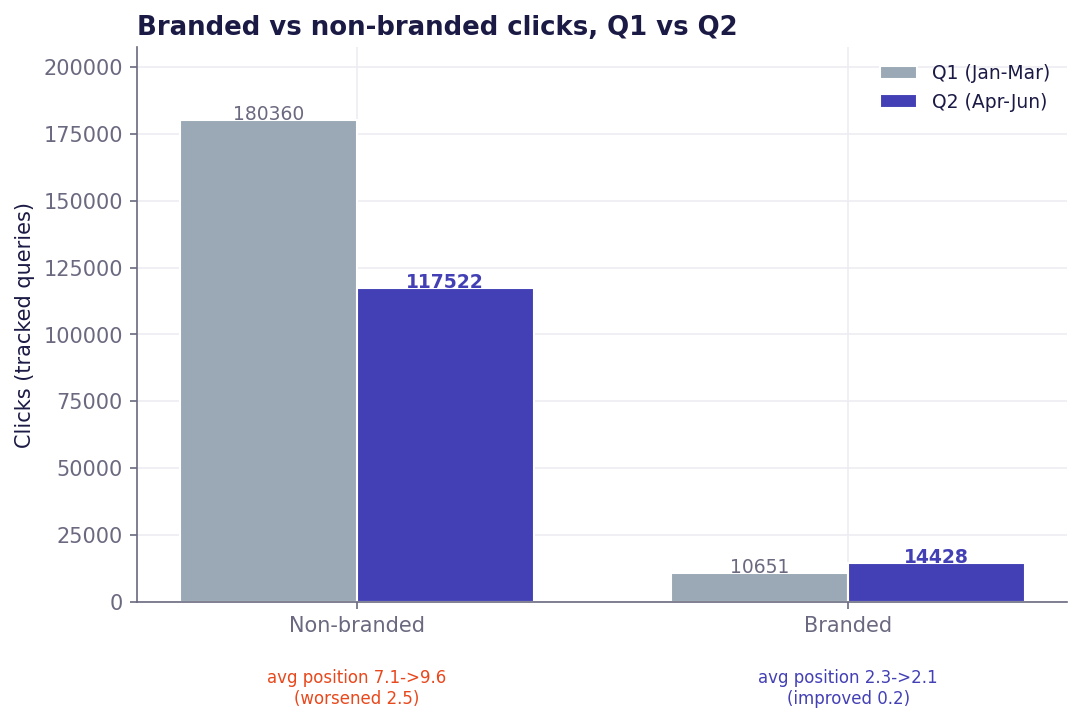

Non-branded search fell; branded search grew.

The whole net decline sits in non-branded queries, where average position also slipped. Branded demand grew 35% and held its top position, so the trust and recall side of the funnel is intact.

| Segment | Clicks: Q1 → Q2 | Change | Avg position |

|---|

| Non-branded | 180,360 → 117,522 | −35% | 7.1 → 9.6 (worsened) |

| Branded | 10,651 → 14,428 | +35% | 2.3 → 2.1 (improved) |

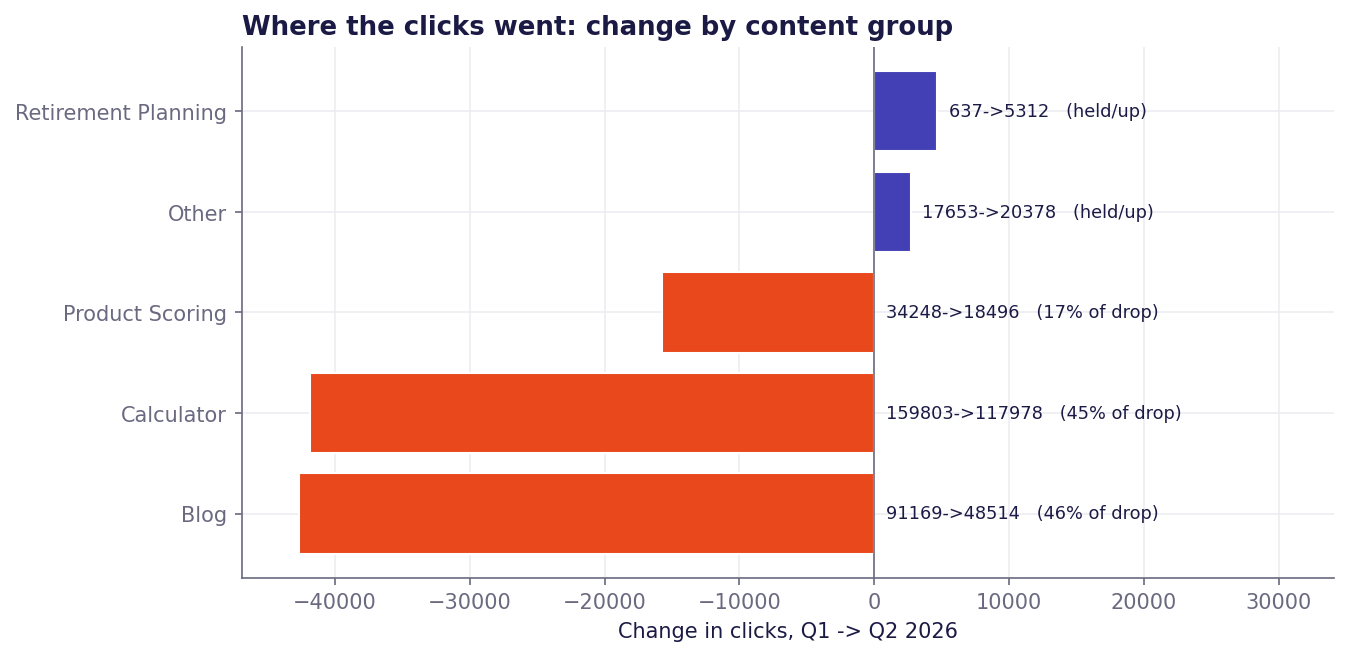

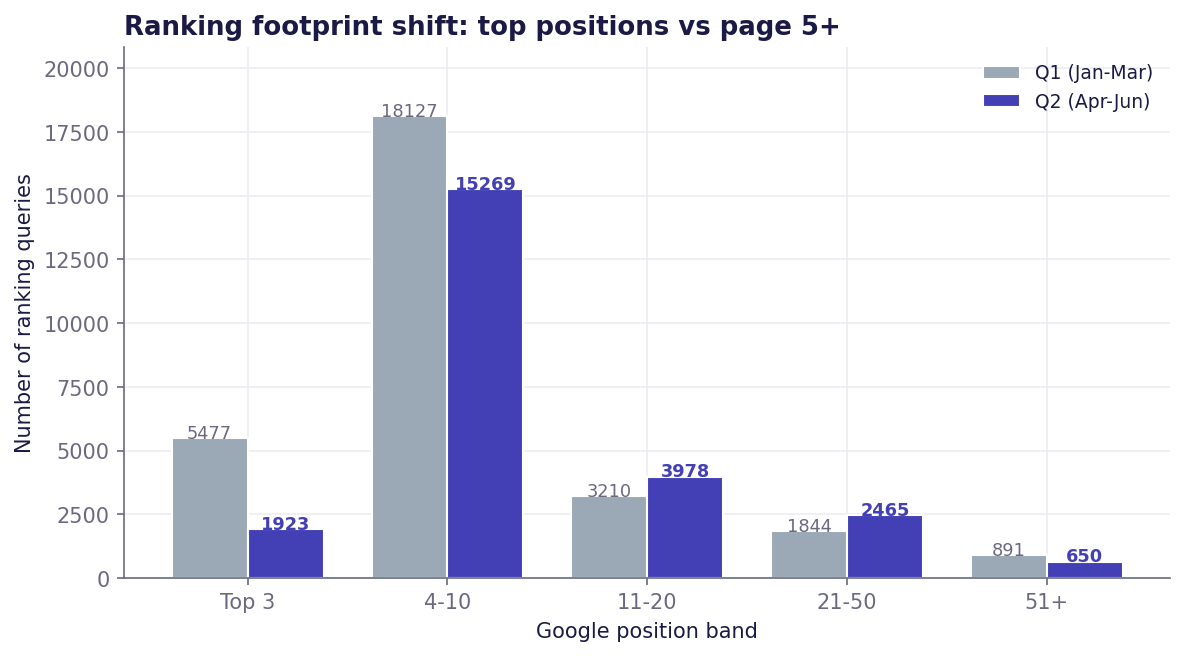

The ranking footprint slipped, but the top pages held

Queries ranking in the top three positions fell nearly two thirds (5,477 to 1,923), redistributing to page two and beyond. Yet when we checked the highest-traffic decliner pages against their own key terms, 12 of 15 held their rankings, so for those pages the clicks left without the rank moving.

| Google position band | Queries in Q1 | Queries in Q2 |

|---|

| Top 3 | 5,477 | 1,923 |

| 4 to 10 | 18,127 | 15,269 |

| 11 to 20 | 3,210 | 3,978 |

| 21 to 50 | 1,844 | 2,465 |

| 51+ | 891 | 650 |

01Zero-click and AI answers

Non-branded "what is" and "how to" queries are increasingly answered on the results page, so a page can hold rank and still lose the click.

02Seasonal tool demand

Tax calculators and regime comparisons peak in the January-to-March tax-planning quarter and recede afterwards. A quarter-on-quarter view always shows that swing.

03Real ranking loss on the mid-tail

Beyond the top pages, the broad Blog mid-tail did lose position, shown by the top-three collapse above. This part is recoverable with on-page work.

04Brand strength is intact

Branded clicks and rankings grew. The opportunity is recapturing non-branded discovery, not repairing brand demand.